Show Notes

S2 E6: This episode might be one of the most controversial because it will challenge the view that dividends and income are meaningful when it comes to investing. Many investors find these to be a vital component of their investment strategy, but Jeff Harrell provides his take on why the yield of an investment is completely irrelevant to him.

Jeff provides examples of investors who swear by dividends, but offers research-backed evidence, as well as personal experience, as to why those beliefs are irrational and ignore the impact of inflation.

Listeners should be prepared to hear a critical take on a popular investing strategy and why it may be more bark, than bite.

(Season 2 Episode 6)

Resources Mentioned in Episode:

Morningstar article, “There Is Nothing Special About Dividends”

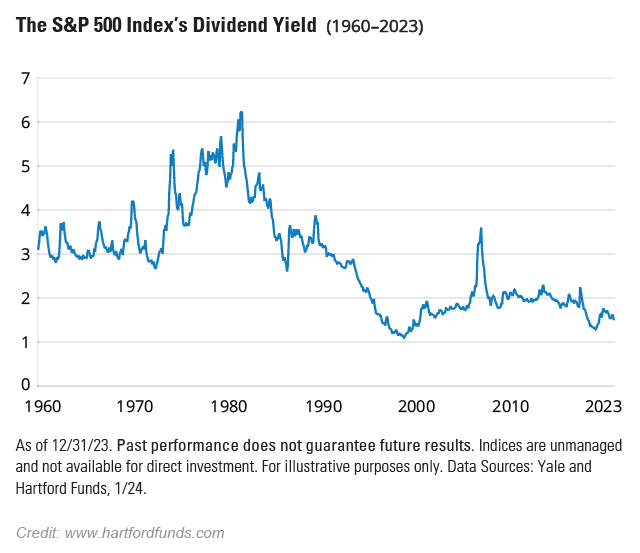

Chart illustrating S&P 500 historical dividend trend:

Podcast produced by Ted Cragg of QuickEditPodcasts.com

Music Credit: Dream Cave / Adventure Awaits / courtesy of www.epidemicsound.com

Transcript

What’s the dividend yield? Or, how much income does that security produce? I used to get these questions all the time from clients when they were asking about the investments in their accounts. Now, to the average investor I get how this might seem like something that is important to know, but my response to questions like this was always the same….Who cares?

Welcome to the second season of Invested Poorly: Sad Tales of FInancial Fails, a short-form podcast designed to help everyday investors make wiser investment decisions by learning what NOT to do with their money. Host Jeff Harrell shares timeless stories from his former life as a financial advisor, about the poor—and irrational—choices he witnessed investors make that disrupted their journey to financial independence, or FI. Your ability to recognize, and avoid, similar mistakes could make all the difference for you along your path to reach FI.

Check out the “Introduction” episode for more background on Jeff, why he created this podcast, and how it can guide you to becoming the hero of your own investing story. Now, on with show.

When it comes to individual stock investing, if I had to pick one question I got asked more often than any other during my career as a portfolio manager, it was definitely, “What’s the yield?” No lie, I would pretty much chuckle every time I got the question because I never knew the answer. Never!!

This response may come as a shock to some of you listening because income and dividends are typically considered important things to consider when it comes to investing. The facts bear this out. Historically, dividends have accounted for roughly one-third of the total return of the stock market. However, if you look at the last couple of decades, this has been steadily declining. I’ve included a chart in the show notes that illustrates this, if you want to check it out for yourself.

In my opinion, the reason for this decline in dividends is because corporate America now places significantly more importance on reinvesting in their business, versus giving money directly to their shareholders. The world has changed a lot over the past couple of decades. Trading fees are significantly lower, access to information is easily available to all investors, and brokerage firms are just better and more efficient when it comes to helping investors manage their investments, which makes sending dividends to shareholders way less important than it used to be. However, what hasn’t changed for some investors is how dividends make them feel.

Often, but not always, this feeling of importance an investor places on dividends comes from investors who are living off their assets. The idea of only spending the income your portfolio produces is extremely attractive to people in this situation. The problem with this thought process is that it’s very short-sighted. And that’s because while it may feel good to look at all the income your portfolio is producing when you reach FI, beating inflation is what you really should be focused on.

If you are unaware just how big a factor inflation is to your FI path, ask your parents or maybe even your grandparents how much gas was when they first got their driver’s license. Or maybe what they paid for their first car. Heck, they might even remember how much simple things like milk or eggs cost when they were kids. This should make you realize that if you are pursing FI and planning to spend multiple decades living off your assets, the price you will be paying for everything will be significantly higher as you reach those later years. Thus, simply replacing your current level of spending today with the income your portfolio is generating will be woefully short at some point down the road.

If those examples don’t convince you that focusing too closely on dividends and income is a bad idea, I have another resource for you to check out. Morningstar released an article I really like which questions the value of dividends. I’ve included a link in the show notes to the full article. The conclusion sums up the research perfectly. It states:

“First, there is nothing special about dividends except that they are a tax-inefficient way to return capital to shareholders, and they are certainly not income (except from a tax perspective); they are just a return of capital. Second, investors are better served by focusing on investing in strategies that provide exposure to the factors they want to invest in. A focus on dividends, whether dividend growth or high-dividend yield, is not likely to add value.” That is a word-for-word quote from Morningstar research.

All I can say now is if you still need more proof dividends are of little importance when it comes to selecting an investment, let me give you an example of how I used to address this when I was a financial advisor. As I already mentioned, I had multiple clients who loved buying securities that produced high levels of income because it made them feel good. These included Real Estate Investment Trusts, Master Limited Partnerships, utilities, high-yield stocks, the list goes on. Whenever I had a client who wanted to invest in these, I’d set up a separate account to allow them to purchase whatever they wanted, so they could see for themselves how the stocks they chose performed, in comparison to the traditional stock investments we would recommend.

Now of course, there were periods where this strategy worked very well, but my personal experience was always the same. Sometimes it took months, quarters, or even more than a year, but eventually the strategy focused on dividends and income would underperform. It didn’t happen every time, but usually the client would eventually throw in the towel and put everything in more traditional investments.

So, one final comment I’ll make before I end this discussion on dividends is to recognize that a final hurdle to overcome with respect to dividends stares back at you every time you look at your accounts. Whether you are reviewing them online or via your monthly statements, brokerage firms are notorious for listing the yield of every security in your account. This will inevitably lead to mental comparisons of all the securities in your accounts, which can result in misguided investment decisions.

These decisions tend to happen most often when the yield is above average. This is because it creates a false sense of confidence in the security, since it seems like such a good investment. I always tell people that whenever an investment has a yield that seems too good to be true, it’s almost always because it is extremely risky or in financial trouble. Trust me, there is no free lunch when it comes to investing.

So, now it’s your call when it comes to dividends and income. If you still think they are important and make you feel good, then by all means, keep doing what you are doing. But, for my money and my plan to live off my assets for the next 50 years, they remain completely irrelevant.

I sure hope you enjoyed this episode of Invested Poorly and will be able to take something from it to improve your decision making as you navigate the twists and turns of your personal investing adventure. Be sure to check out my website at AreYouFI.com (that’s A R E Y O U F I dot com) where you can find resources and show notes with the charts and graphs I mention during the episodes. These are like little treasure maps that can help you choose more wisely along your quest to reach FI, or financial independence.

Never forget, in the short-term the stock market is unpredictable, and as my mischievous little nephew likes to say, “things just happen”! So focus on the long-term, by controlling your emotions, simplify your investments, and always… ignore the noise.

I’m your host, Jeff Harrell. Thanks for listening.

Invested Poorly: Sad Tales of FInancial Fails was created for informational purposes only and should not be relied on for specific tax, legal, or investment advice. You should consider consulting a qualified professional to review your situation before engaging in any transactions. Investing involves risk, including loss of principal and past performance is no guarantee of future results.

This podcast was produced by Ted Cragg. Learn more about creating podcast mini-series like this by visiting QuickEditPodcasts.com.