Show Notes

S2 E10: Speaking especially to people who are sensible with their finances and live within their means, Jeff Harrell discusses one of the greatest fears all investors face, longevity. While this fear is real for many, experience suggests these fears are likely irrational for those who act in fiscally responsible ways throughout their lifetime.

You’ll hear stories of encouragement to spend more after attaining financial independence, as well as the simple FI budget strategy Jeff uses personally to ensure he optimizes his spending now that he is FI.

This episode offers the listener an opportunity to develop a FI mindset, providing confidence all the hard work in the early years will pay off.

(Season 2 Episode 10)

Resource Mentioned in Episode:

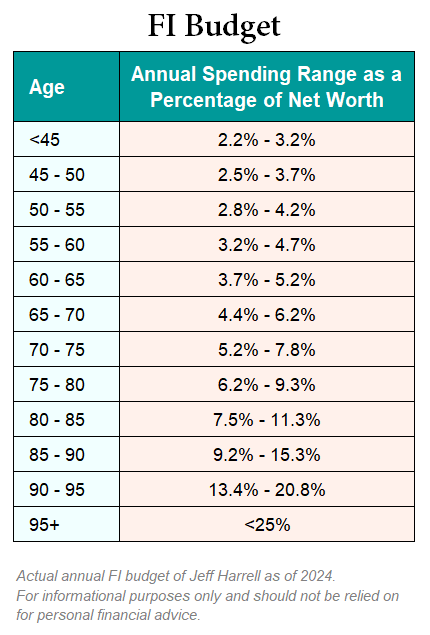

FI Budget (target annual spending percentages):

Podcast produced by Ted Cragg of QuickEditPodcasts.com

Music Credit: Dream Cave / Adventure Awaits / courtesy of www.epidemicsound.com

Transcript

Based on countless surveys I’ve read over the years, more Americans are afraid of running out of money than dying. Honestly, this fear makes perfect sense to me. I can totally see how spending the final years of your life in an uncomfortable situation that is beyond your control sounds like a horrible way to live out your final days. And so, while there is no doubt many Americans are currently, or will be, in this unfortunate situation, for those of you listening who are financially responsible, my bet is not only will you never run out of money, but more than likely you won’t even come close.

Welcome to the second season of Invested Poorly: Sad Tales of FInancial Fails, a short-form podcast designed to help everyday investors make wiser investment decisions by learning what NOT to do with their money. Host Jeff Harrell shares timeless stories from his former life as a financial advisor, about the poor—and irrational—choices he witnessed investors make that disrupted their journey to financial independence, or FI. Your ability to recognize, and avoid, similar mistakes could make all the difference for you along your path to reach FI.

Check out the “Introduction” episode for more background on Jeff, why he created this podcast, and how it can guide you to becoming the hero of your own investing story. Now, on with show.

One. That’s the number of clients I worked with over my two-decade career who actually ran out of money. It was the mother of a doctor and let’s just say, she was living well above her means for years before her net worth dropped to $0. Now before you feel sorry for her, I should add some context. She knew without a doubt that her son, the doctor, would take care of her if she ran out of money. I had spoken to him many times over the years, and he always said he just wanted her to be comfortable.

So in reality, this is a story of a son who loved his mother so much, he wanted her to live life to the fullest for as long as she remained with us, even at his expense. I realize this scenario may not be an option for everyone listening, but the point I’m going to try and make in this episode is how rare running out of money actually is for those who are fiscally responsible.

Other than this situation, I never once had a client run out of money or quite frankly even come close. And the reason for this is pretty obvious when I think about it.

First, I will admit the firm I worked for serviced individuals who had the capacity to save a sizeable portion of their income for the future. So it’s totally fair to assume most of my clients were at least somewhat financially responsible.

Second, nearly all of the individuals I worked with wanted to be financially prepared to make their money last well into their 90s. This combination of a focus on saving in your younger years, while preparing for an outcome that probably less than 20% of Americans ever reach (which is living past the age of 90) tends to result in more money than you can possibly spend, even if you end up living that long.

Now, before I go any further, I want to reiterate that I’m speaking to a very specific audience in this episode. That being, fiscally responsible individuals who live within their means. My assumption is if you are listening to this podcast, this probably describes you. Which is why my goal of this episode is to help you not only feel confident you will reach FI, but even more importantly, feel comfortable spending your money when you get there.

One story right up this alley involves a retired couple who called me up to ask if they could afford to take a two-week trip to Europe. It was something they had always wanted to do, but never found the time to do it. They had been doing all sorts of research on different tours and eventually settled on one that had everything they were looking for. They told me over and over again how much they wanted to go, but then said they weren’t sure if they could afford it.

Obviously, the next question I asked them was, how much is it going to cost? I think all in, flights, tours, food, gratuities, everything they could think of would be somewhere around $15,000. I almost laughed out loud because not only was this so far within their budget, I couldn’t believe they somehow thought they might not be able to afford it.

You see, this particular client was retired military, and his spouse was a former teacher. They both had pensions and the best medical coverage possible due to his veteran status. They honestly never touched their investments because their pensions already covered more than they spent annually. I think their liquid investments were somewhere around $2 million and they were both in their early 70s.

You don’t need to be a financial advisor to figure out that a $15,000 trip to Europe isn’t going to hurt their retirement one bit. In fact, I remember using this conversation to encourage them to spend more money and really enjoy the fruit of all their labor over the years. However, this is a perfect example of how individuals who are financially responsible their whole lives tend to have a difficult time actually spending money after they reach FI.

Another example I have hits about as close to home as possible. That would be how my wife and I go about spending our money. If you are not already familiar with our story, you can read the details about how we achieved FI in our mid 40s on our website, AreYouFI.com. We are now living 100% off our investments, with absolutely no earned income.

The way we determine our annual FI budget is by using a targeted spending range based on our age and a percentage of our net worth. I’ve included this information in the show notes so you can see the exact spending ranges we use to determine our annual FI budget. The targeted spending ranges increase as we get older because we have less potential time in front of us.

What I love about this strategy is that it’s highly adaptive to market conditions and automatically adjusts your FI budget based on your age. The specific details of exactly how I came up with our spending percentages are beyond the scope of this podcast and honestly not that important. Instead, what’s more important is understanding the concept of how to set your FI budget, which I’d like to try and explain.

First, I think we can all agree if your current annual spending is less than 1% of your net worth, you have an almost 0% chance of ever running out of money, regardless of how old you are. I mean, it would take you 100 years to spend all your money; admittedly this does not account for inflation, but still, in this situation you are clearly FI and no longer need any earned income to maintain your lifestyle.

On the flip side, if you are spending over 10% of your net worth every year, it is extremely likely that—unless you are already advanced in age, say in your mid-80s—you will undoubtedly deplete your net worth if you live into your 90s, and therefore you are clearly not FI. In this example, you most definitely need to keep working until your annual spending drops to a more reasonable percentage of your net worth.

So I hope these hypothetical examples make it crystal clear that the safe level of annual spending after reaching FI falls somewhere between 1% and 10% of your net worth. If you can follow my logic here, then the targeted spending ranges I use to determine my FI budget annually, should provide you with a good example of what annual spending level you can justify, based on your age and net worth, to live a comfortable FI life. Again, you can find my annual FI budget spending ranges in the show notes. And make no mistake about it, I’m putting my money where my mouth is because I’m counting on this to work for me over the next 50 years. And as my adorable little niece would say, “that’s a long time!”

I sure hope you enjoyed this episode of Invested Poorly and will be able to take something from it to improve your decision making as you navigate the twists and turns of your personal investing adventure. Be sure to check out my website at AreYouFI.com (that’s A R E Y O U F I dot com) where you can find resources and show notes with the charts and graphs I mention during the episodes. These are like little treasure maps that can help you choose more wisely along your quest to reach FI, or financial independence.

Never forget, in the short-term the stock market is unpredictable, and as my mischievous little nephew likes to say, “things just happen”! So focus on the long-term, by controlling your emotions, simplify your investments, and always… ignore the noise.

I’m your host, Jeff Harrell. Thanks for listening.

Invested Poorly: Sad Tales of FInancial Fails was created for informational purposes only and should not be relied on for specific tax, legal, or investment advice. You should consider consulting a qualified professional to review your situation before engaging in any transactions. Investing involves risk, including loss of principal and past performance is no guarantee of future results.

This podcast was produced by Ted Cragg. Learn more about creating podcast mini-series like this by visiting QuickEditPodcasts.com.