Show Notes

S2 E8: Maintaining total control of your finances starts with something that seems simple and yet tends to be a major hurdle for many of us to overcome. Discover the importance of organizing your investment accounts and how merely knowing where all your money is located can lead to better investment results in the long term.

Jeff Harrell shares more stories from the trenches of financial planning that illustrate why the negative effects of putting off your financial “to-do list” for a few more months or maybe even years will only worsen the longer you wait.

This episode is designed to get you to stop procrastinating and start taking action with some small steps that will make a big impact on your FI journey.

(Season 2 Episode 8)

Resource Mentioned in Episode:

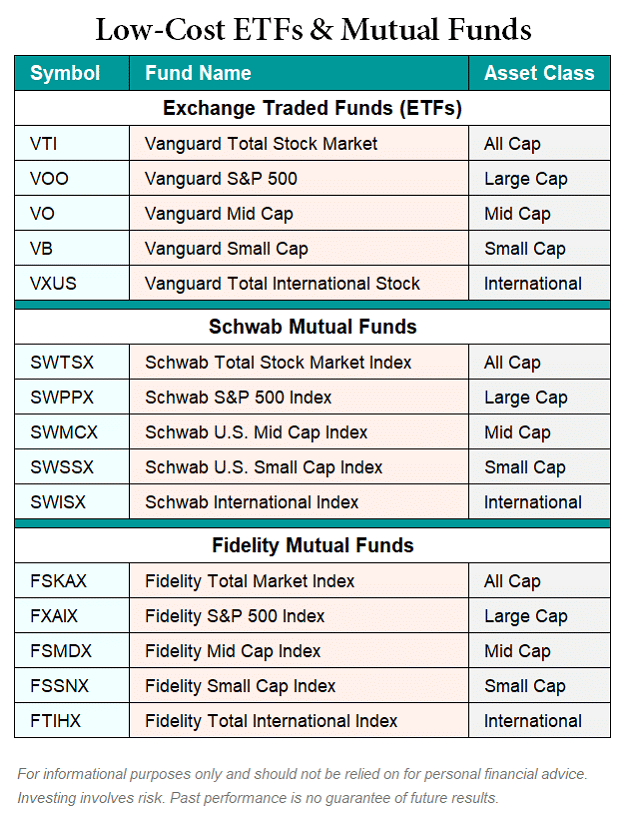

A list of index exchange traded funds (ETFs) to consider if your custodian doesn’t charge transaction fees for each purchase, and no-fee index mutual funds offered by custodians Schwab and Fidelity in various asset classes:

Other Episode Referenced:

Podcast produced by Ted Cragg of QuickEditPodcasts.com

Music Credit: Dream Cave / Adventure Awaits / courtesy of www.epidemicsound.com

Transcript

Have you ever grabbed a jacket out of the closet and found money in one of your pockets? Even though it was already your money, it feels like free money, since you didn’t realize you had it, right? Now imagine if something like this happens with your investments. I kid you not, I’ve met people who didn’t realize they had 10, 50, even more than 100 thousand dollars in an account that they had completely forgotten about. And while the idea of finding your own money does have some appeal, which I totally get, what it actually means is you probably could have reached FI a little sooner.

Welcome to the second season of Invested Poorly: Sad Tales of FInancial Fails, a short-form podcast designed to help everyday investors make wiser investment decisions by learning what NOT to do with their money. Host Jeff Harrell shares timeless stories from his former life as a financial advisor, about the poor—and irrational—choices he witnessed investors make that disrupted their journey to financial independence, or FI. Your ability to recognize, and avoid, similar mistakes could make all the difference for you along your path to reach FI.

Check out the “Introduction” episode for more background on Jeff, why he created this podcast, and how it can guide you to becoming the hero of your own investing story. Now, on with show.

One of the first things a financial advisor will do when meeting with a prospective client is ask them for their current financial statements. This was always one of my favorite parts of the business because you get to see how different we all are when it comes to managing our money. While some people are on top of it and know exactly where every penny is, which I’m guessing describes many of you listening right now, as you can probably imagine, I’ve seen many situations over the years that would make your head spin when it comes to how some people keep track of their investments.

One of my favorite things to do when a prospective client had accounts at multiple custodians was to spread out their paper statements on our conference room table so they could see how their money was all over the place. It never ceased to amaze me how often people had no clue what a specific account was or where it came from when I would start asking questions about a particular statement.

While I do understand there are a host of reasons why someone might have accounts at multiple locations, one of the greatest values I believe I provided for my clients was simply consolidating their accounts. The benefits go much further than just being able to track your investments more easily. Without question, you can reduce fees and taxes by improving your account organization.

One situation I witnessed frequently during my time as a financial advisor occurs when you leave or change employers. Nowadays, it is very common to have a retirement plan that needs to be transferred after you are no longer working there. It was absolutely shocking to me how often people would somehow forget about this, or even intentionally ignore it because it seemed too confusing to deal with. I’m guessing some of you listening may be guilty of this as well. So if you are in this situation, I hope this episode encourages you to figure out how to get your retirement plan accounts consolidated and fully under your control.

The most extreme example I saw of this involved a couple I met who had asked for a review of their financial situation. They sent me their statements and I remember the first meeting with them because it was obvious neither of them had prioritized managing their investments. This was one of those meetings where I papered our conference room table with their statements and started asking them questions. One statement that stood out was a six-figure account that neither of them knew where it came from.

So, I’m dead serious when I tell you that after they became clients, I had to do the research to figure out exactly what type of account it was and how it could be consolidated into an account they would have more control over. While they were super appreciative of this, the sad part is, this account had been sitting there bearing almost no interest for nearly a decade. I mean, I guess you can say this was a good thing that I was able to help them get their account invested, but think of the missed opportunity they had with this money.

Another story of investment neglect comes from a friend of mine who texted me out of the blue one day with a picture of a statement. I think the text went something like, “hey look what I just found!” It was an IRA worth around $30,000. He pretty much threw himself under the bus saying he kind of knew about it, but really hadn’t thought about it for years. He was asking me what he should do with it. Fortunately, this one has a much happier ending.

I took a look at the statement for him and although it was invested in an actively managed mutual fund, the performance had been above average over the past ten years, which is to say it did better than most other actively managed mutual funds. But it still had underperformed a total stock market index fund. Thus, his lost opportunity was minimal, but not insignificant. Had this gone on for another decade or more, we could easily be talking about an extra year or so for him to reach FI. This is just another example of how important it is to keep track of your investments.

I also saw benefits over the years from consolidating accounts in the form of tax savings. If you lose track of how much money you have in your various account types, you won’t be able to optimize your investments. If you haven’t done so already, be sure to listen to Episode 5 of Season 2 on asset location where I discuss how simply purchasing the right investments in the right account types can lower your tax burden tremendously. This is so much easier and more efficient to do when you have consolidated your investments.

Now, if you are looking for advice about where to consolidate your accounts, I would recommend you check out Schwab and Fidelity. I personally use Schwab and I am very happy with everything they have to offer. I’ve never used Fidelity for my own money, but I have a number of friends who have, and my experience with helping them manage their investments at Fidelity is that it’s comparable to Schwab. Both custodians offer pretty much every service a traditional investor could need, and I think both of their online interfaces are user-friendly. As with anything, there is always a learning curve when you try something new, but I think you will be able to confidently navigate either platform relatively quickly.

Perhaps the most valuable feature both Schwab and Fidelity offer is no transaction fees for stock and ETF trades. Without question, reducing your fees to as close to zero as possible is super important, and both custodians offer the ability to do just that. It’s also crucial to understand both custodians offer their own mutual funds that charge no transaction fees when buying or selling.

So, if you prefer to use mutual funds for your investments, be sure to check out this episode’s show notes for a list of index mutual funds offered by both custodians in various asset classes. On the other hand, if you prefer using ETFs, I’ve also included in the show notes a list of index ETFs you may want to consider if your custodian doesn’t charge transaction fees for each purchase.

If you are not sure what the difference is between a mutual fund and an ETF, which stands for exchange traded fund, take my inquisitive little nephew’s advice and “search it up.” It is extremely important that you understand the difference between these investment vehicles, and which one is optimal for your specific situation.

So, if you are one of those people who has been putting off consolidating your accounts because of the potential headaches, hopefully this episode will give you the nudge you need to move forward. As you can see, the longer you wait, the more detrimental the ramifications could be to your finances.

I sure hope you enjoyed this episode of Invested Poorly and will be able to take something from it to improve your decision making as you navigate the twists and turns of your personal investing adventure. Be sure to check out my website at AreYouFI.com (that’s A R E Y O U F I dot com) where you can find resources and show notes with the charts and graphs I mention during the episodes. These are like little treasure maps that can help you choose more wisely along your quest to reach FI, or financial independence.

Never forget, in the short-term the stock market is unpredictable, and as my mischievous little nephew likes to say, “things just happen”! So focus on the long-term, by controlling your emotions, simplify your investments, and always… ignore the noise.

I’m your host, Jeff Harrell. Thanks for listening.

Invested Poorly: Sad Tales of FInancial Fails was created for informational purposes only and should not be relied on for specific tax, legal, or investment advice. You should consider consulting a qualified professional to review your situation before engaging in any transactions. Investing involves risk, including loss of principal and past performance is no guarantee of future results.

This podcast was produced by Ted Cragg. Learn more about creating podcast mini-series like this by visiting QuickEditPodcasts.com.