Show Notes

S1 E7: Timing the stock market is something we’re all told not to do, yet all of us are guilty of it at some point. This episode may have the “smoking gun” illustration to help you avoid this poor decision going forward.

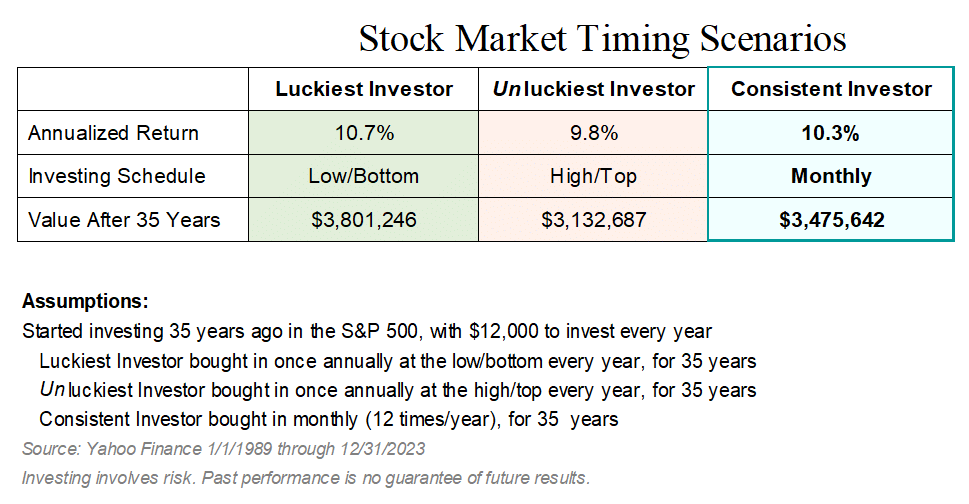

Jeff Harrell explains two hypothetical (and impossible) scenarios of the luckiest and unluckiest investors in history—the former buying into the stock market at the very bottom every year and the latter buying in at the very top. How wide do you think the gap is between their portfolio values after a 35-year time horizon?

He adds a third (and more realistic) scenario of an investor dollar cost averaging into the market monthly, instead of annually, and compares their portfolio to those of the world’s luckiest and unluckiest investors.

Don’t answer the following question until you’ve heard this episode: “Is now a good time to invest in the stock market?”

(Season 1 Episode 7)

Resource Mentioned in Episode:

Data illustration of hypothetical stock market timing scenarios:

Other Episodes Referenced:

Podcast produced by Ted Cragg of QuickEditPodcasts.com

Music Credit: Dream Cave / Adventure Awaits / courtesy of www.epidemicsound.com

Transcript

Is now a good time to invest in the stock market? Let’s be honest, this thought has crossed all of our minds at some point in time. I get it. We all do it. It’s totally natural. Some of this is just human nature, but I think in today’s world it is even more a function of the 24/7 news environment we live in, bombarding us with so much information. I mean, the sheer volume of news we have thrown at us on a daily basis can easily paralyze us when it comes to taking action with our investments. Well, if you’ve got just a couple minutes to hear me out, I think I might be able to convince you that the answer to “Is now a good time to invest in the stock market,” is always…YES.

Welcome to the first season of Invested Poorly: Sad Tales of FInancial Fails, a short-form podcast designed to help everyday investors make wiser investment decisions by learning what NOT to do with their money. Host Jeff Harrell shares timeless stories from his former life as a financial advisor, about the poor—and irrational—choices he witnessed investors make that disrupted their journey to financial independence, or FI. Your ability to recognize, and avoid, similar mistakes could make all the difference for you along your path to reach FI.

Check out the “Introduction” episode for more background on Jeff, why he created this podcast, and how it can guide you to becoming the hero of your own investing story. Now, on with show.

Most of you listening, at some point in time, will experience a situation where you have an opportunity to save a little more money than normal. This might occur due to a raise, bonus, inheritance, maybe you finished paying off some debt; it doesn’t really matter what it is, but for most of us something like this will happen. Inevitably, this triggers that little voice in the back of your head asking, “is now a good time to invest?” If you are ready, I’m going to enlighten you on how I think you should react the next time this thought pops into your head.

About halfway into my career as a financial advisor, I stumbled upon a research report that I honestly didn’t believe could be accurate until I ran the numbers myself. I’m going to try and explain the results of these calculations in this episode.

So here’s how the scenario goes. Suppose you started investing 35 years ago in the S&P 500 and you were the luckiest person in the history of the world. You had $12,000 to invest every year and you bought at the bottom of the market every single year, for 35 straight years. If you were this lucky, you would have $3.8 million dollars today, which works out to about a 10.7% annualized return. Not bad, right?

However, we know that’s impossible, so for fun, let’s suppose something else just as impossible occurred. Instead of picking the bottom every year, let’s say the opposite happened. This time you invested $12,000 a year for 35 years, but instead of buying at the bottom every year, you bought at the top of every year. The result this time…you would now have $3.1 million dollars. Roughly $700,000 less. Now, don’t get me wrong, I know $700,000 is a lot of money, but when you think about each scenario, which are both impossible, the gap doesn’t actually seem that wide to me.

So, instead of the two impossible scenarios, now let’s imagine a third scenario, that is significantly more realistic. Let’s say that, instead of investing $12,000 once every year, you invested $1,000 a month, every month, for 35 years. The outcome this time…a little under $3.5 million dollars. It works out to about $325,000 less than the perfect (yet impossible) timing scenario and about $350,000 more than the worst possible timing scenario. Trust me, the numbers are correct.

I can’t even begin to tell you how often I would use this example when speaking with clients who were thinking of timing the market. I’ve used this so many times I feel like a broken record explaining it, but the first time you hear it can profoundly affect how you look at investing. I even had an advisor one time follow up with me a couple days after he heard me mention this. He said he did the same thing I did; he downloaded all the data and ran the numbers himself because he was skeptical. He figured I must’ve calculated something incorrectly. I bet he’s probably out there now telling this story the same way I do.

All I can say is that if this example doesn’t make it crystal clear that trying to time the market is pointless, then I don’t know what will. Keep in mind, the results of this study are over a very, very long-time horizon, so please don’t misinterpret the conclusion I’m trying to draw here by somehow thinking stocks will go up every year. Not at all; that is not what I’m saying.

In episode 4, I talk about volatility and risk, providing more detail on what investors can expect over time periods much shorter than 35 years. So be sure to check out episode 4 to gain further clarity on this point. Also, I want to make sure you understand this example assumes we are talking about your investments, not savings. In episode 3, I discuss the difference between investing and saving, so be sure to listen to that episode as well.

Hopefully this episode has given you some food for thought, so the next time you have a pile of money to do something with and you ask yourself, “is now a good time to invest?”, you’ll answer the same way I always do.

I sure hope you enjoyed this episode of Invested Poorly and will be able to take something from it to improve your decision making as you navigate the twists and turns of your personal investing adventure. Be sure to check out my website at AreYouFI.com (that’s A R E Y O U F I dot com) where you can find resources and show notes with the charts and graphs I mention during the episodes. These are like little treasure maps that can help you choose more wisely along your quest to reach FI, or financial independence.

Never forget, in the short-term the stock market is unpredictable, and as my mischievous little nephew likes to say, “things just happen”! So focus on the long-term, by controlling your emotions, simplify your investments, and always… ignore the noise.

I’m your host, Jeff Harrell. Thanks for listening.

Invested Poorly: Sad Tales of FInancial Fails was created for informational purposes only and should not be relied on for specific tax, legal, or investment advice. You should consider consulting a qualified professional to review your situation before engaging in any transactions. Investing involves risk, including loss of principal and past performance is no guarantee of future results.

This podcast was produced by Ted Cragg. Learn more about creating podcast mini-series like this by visiting QuickEditPodcasts.com.