Show Notes

S3 E1: The three investment phases we all go through are accumulation, transition, and drawdown. This episode explains how to invest during each phase and what changes you should make as you shift from one phase to the next.

Host Jeff Harrell shares his unique strategy to navigate all three phases. Using his personal FI journey as a guide, you will be able to steer your own path to FI success based on your specific situation.

In less than 15 minutes, you’ll learn how to manage a portfolio over multiple decades and life changes. Simplifying your portfolio and having a strategy based on your stage of life, not market conditions, should lead to peace of mind when it comes to managing your investments.

(Season 3 Episode 1)

Resources Mentioned in Episode:

Cody Garrett (Measure Twice Money) video, "Retirement Savings Order of Operations"

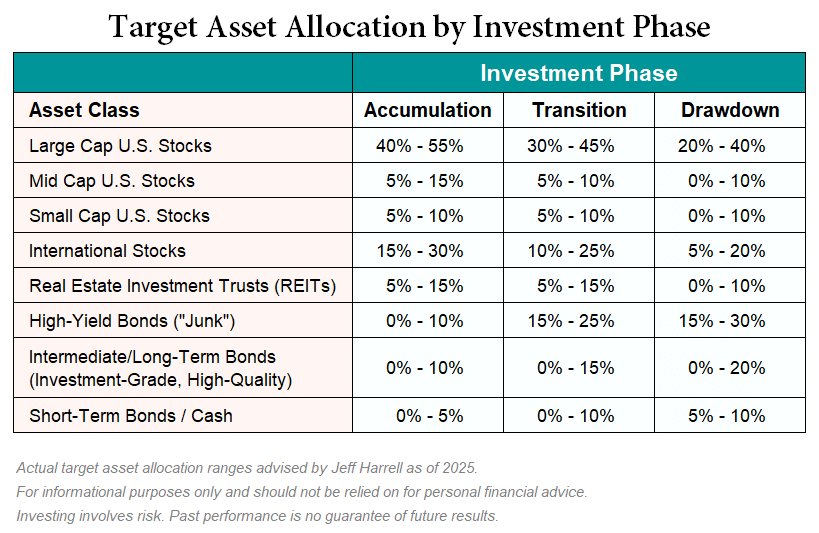

Target Asset Allocation by Investment Phase table - illustrates recommended target asset allocations by asset class during the three investment phases of Accumulation, Transition, Drawdown

Other Episodes Referenced:

Podcast produced by Ted Cragg of QuickEditPodcasts.com

Music Credit: Dream Cave / Adventure Awaits / courtesy of www.epidemicsound.com

Transcript

Making portfolio adjustments is one of the most common and important things a wise investor can do over the course of managing their money. However, while most investors believe these adjustments should be based on market conditions and the economic outlook, I’m here to tell you that whatever is going on with the financial markets, good or bad, should have absolutely nothing to do with the changes you make. The only, and I mean only, reason you should ever make material adjustments to your portfolio is when you enter a new investment phase.

Welcome to the third season of Invested Poorly: Sad Tales of FInancial Fails, now part of the Bold Departure Network. Invested Poorly is a short-form podcast designed to help everyday investors make wiser investment decisions by learning what NOT to do with their money. Host Jeff Harrell shares timeless stories from his former life as a financial advisor, about the poor—and irrational—choices he witnessed investors make that disrupted their journey to financial independence, or FI. Your ability to recognize, and avoid, similar mistakes could make all the difference for you along your path to reach FI.

Check out the “Introduction” episode for more background on Jeff, why he created this podcast, and how it can guide you to becoming the hero of your own investing story. Now, on with the show.

As we get older, things change, and this is certainly true when it comes to our investments. In our 20s and 30s, most of us feel as though we have all the time in the world in front of us and the idea of living off our investments feels like an eternity away. I call this initial phase of your investing journey the Accumulation Phase because you have absolutely no intention of spending the money you’ve invested any time soon.

As we progress through our careers and life changes, we will eventually enter a period where work may no longer be necessary or, in unfortunate cases, is no longer possible. This will look different for all of us, but when this starts to happen, I refer to this second phase as the Transition Phase. You may not know exactly when you will switch from investing extra money to actually spending what you have accumulated, but you can see that it’s coming in the near future.

Third and final is the Drawdown Phase. All those years of hard work, saving and investing, are set to pay off as you now watch your money work for you. Although the length of each phase is different for all of us, the investment strategy isn’t.

If you have listened to any episodes from Season 1 or 2, then you know my experience as a financial advisor suggests most investors are their own worst enemy when it comes to their investments. In the context of this episode about investment phases, what I want to highlight is that most investors focus on the wrong thing. Specifically, they think adjustments to their portfolio should be based on what’s happening with the economy, politics, tech trends, whatever.

Seriously, these factors are irrelevant to me. From my perspective, making any material portfolio adjustments based on news headlines amounts to market timing. And if you need a reminder about why I think market timing is futile, be sure to check out Episode 7 of Season 1.

So instead of focusing on external factors that are completely beyond your control, a proper long-term investment strategy should focus solely on where you are in your stage of life, whether you’re in the Accumulation, Transition, or Drawdown Phase. Unfortunately, I’ve seen what can happen when people don’t understand this concept.

During my career, I experienced numerous corrections and bear markets with my clients. Although volatility is never fun, the secret to getting through the inevitable market drops is having a plan in place to know what you’ll do when—not if—they occur. Being prepared made my client conversations during these times much easier.

I think this is why my most memorable stories during these times do not involve my clients, but instead prospects who came begging for help because their portfolio had dropped dramatically and they didn’t know what to do. Often, these were individuals who had retirement in sight, or so they thought, before a large decline in the stock market.

It was hard to have these conversations because what they wanted was someone to tell them exactly how long the downturn would last and what to do. These prospects never became clients because I wasn’t willing to tell them what they wanted to hear, which was that I could navigate the ups and downs for them perfectly. I was more than happy to let them find another advisor who would promise them that.

Hopefully you now have an idea of what I’m trying to convey in this episode, which is that when it comes to investing, focus on where you are in your stage of life, and with respect to everything else…ignore the noise.

So let’s dive deeper and talk more about the Accumulation Phase. This is the easy one. When you are more than a decade away from achieving financial independence, or FI, save as much as you can while still living a fulfilling life, and invest aggressively. That’s it. That really is all you need to know as far as I’m concerned.

The only other point I’d like to make about the Accumulation Phase is to make sure you understand the savings priority order. A great resource for this is an excellent video on “Retirement Savings Order of Operations” from Cody Garrett of Measure Twice Money. I will include a link in the show notes. This is just one video of many he has created on various investing and financial planning topics, so be sure to check out the Measure Twice Money YouTube Channel because the videos are excellent.

Now, on to the Transition Phase. This phase starts when you realize you are within a measurable amount of time to reaching FI, let’s say 3 to 7 years. It isn’t that important to define exactly when it starts, but it is crucial to recognize that your investing strategy needs to change when you enter the Transition Phase. The way I recommend investors make this change is by adjusting how their current savings are invested. Put simply, start investing all your savings in more conservative investments, with a goal of hitting your desired asset allocation target (which is jargon for your stock-to-bond-to-cash ratio) by the time you fully reach FI.

I’m going to try and keep this as simple as possible, let’s say you have 100% of your investments in a diversified portfolio of stock mutual funds or ETFs. Maybe you want to get to a 20% or 40% bond ratio by the time you reach FI. You can now stop purchasing stocks and invest all your new savings in bonds, with the goal of hitting that target in however many years you think it will take to reach FI.

I love this strategy because it allows you to still hold onto your stock investments and not sell them. It also slowly makes your portfolio more conservative, instead of instantly doing so just because you are getting close to FI. Further, it prevents you from the most common pitfall I saw during my career—leaving your portfolio aggressively invested for too long, which would expose you to extreme risk if a dramatic decline happens right before you reach the Drawdown Phase.

Shockingly, I never saw any advisors recommend a strategy like this during my career, but it makes so much sense, which is why I advise everyone to use the concept as a guide to navigate your transition from accumulation to drawdown.

This now brings us to phase three, by far the most exciting stage of a FI journey, the Drawdown. Ultimately, this is what we are all striving for. Not because you want to be a lazy bum the rest of your life. No, the final phase of FI is when you now have the ability to be “in the moment” at all times because your lifestyle is fully funded by your investments. You are no longer beholden to a job, or boss, or deadlines that aren’t your choice. You are now FI, embrace it and live it to the fullest.

As for your investments during the Drawdown Phase, there are countless strategies out there, many of which have merit in my opinion. None of them are right or wrong, so before I explain mine, I would just like to say make sure you have a strategy during this phase that addresses your specific withdrawal rate, risk tolerance, and factors in the different type of accounts you have. And most importantly, a strategy you can stick with.

That said, I’ve recorded a bonus segment, which is linked in the show notes, where I share a detailed description of my actual investment percentages. The purpose of providing this is not for you to try and make your accounts look identical to mine, but to help you understand how I got from the Accumulation Phase to fully FI. I like to say portfolio management is more art than science, so I’m hoping this will help you paint your own picture of your FI portfolio based on your FI path. The bonus segment will walk you through how my accounts got to where they are today, so check that out if you are interested.

What I also really want to get across before I end this episode is that my investment decisions are based 100% on the target asset allocations I have for each of my investments. As I draw down my portfolio, I try to keep the asset allocations as close to my targets as possible. I do this by no longer reinvesting dividends, which gives me more flexibility to decide what to do with this money.

When these hit, the dividends get invested in either stocks, bonds, or cash, whichever asset class is most underweight its target. Usually, that is the cash allocation because I’m obviously spending that cash portion of my portfolio every month. But if the market takes a big hit, I may buy stocks or bonds because those assets might have dropped enough to bring my cash allocation above its target weight. This is how you take advantage of market dips during the FI Drawdown Phase. I only buy more stocks after a sharp market decline. Again, be sure to check out the bonus segment I mentioned earlier if you are more interested in the nitty gritty details of my investment strategy.

Finally, I’ve included a table that provides target asset allocations by asset class during the various investment phases I discussed during this episode. Use these as a guide to help determine your investing path to FI and the adjustments you should make at various points in time. Reaching FI is a decade-long-plus goal for most of us and as my adorable, yet impatient, little niece likes to say, “that’s a long time.” I can only speak for myself, but the over two decades of fiscal responsibility, a focus on saving money, and good investing, was totally worth it to achieve a life of freedom which now allows me to always be “in the moment.”

I sure hope you enjoyed this episode of Invested Poorly and will be able to take something from it to improve your decision making as you navigate the twists and turns of your personal investing adventure. Be sure to check out my website at AreYouFI.com (that’s A R E Y O U F I dot com) where you can find resources and show notes with the charts and graphs I mention during the episodes. These are like little treasure maps that can help you choose more wisely along your quest to reach FI, or financial independence.

Never forget, in the short-term the stock market is unpredictable, and as my mischievous little nephew likes to say, “things just happen!” So focus on the long-term, by controlling your emotions, simplify your investments, and always… ignore the noise.

I’m your host, Jeff Harrell. Thanks for listening.

Invested Poorly: Sad Tales of FInancial Fails was created for informational purposes only and should not be relied on for specific tax, legal, or investment advice. You should consider consulting a qualified professional to review your situation before engaging in any transactions. Investing involves risk, including loss of principal and past performance is no guarantee of future results.

This podcast was produced by Ted Cragg. Learn more about creating podcast mini-series like this by visiting QuickEditPodcasts.com.